New information and evidence were released by the Independent Authority for Public Revenue (AADE) regarding organized financial-crime rings dismantled over the past week. The rings used “straw men” to manage dozens of shell companies in the food service and nightlife sector.

In a detailed, multi-page presentation, the AADE explains how the operational action—codenamed “Straw Men”—unfolded and led to the identification of three large rings with combined debts of more than €24 million in taxes and social-security contributions.

Starting point: inspections of food-service chains

According to the information and specialized charts, the first suspicious indications were detected in Attica. The investigation began with joint operations by mixed AADE audit and collection teams at food-service and entertainment businesses in the region.

Inspectors focused on compliance with labor legislation, the legality of alcohol distribution, and adherence to registration obligations in the Register of Beneficial Owners.

A critical finding was that chains of outlets were operated through different legal entities rather than a single corporate entity. During inspections, authorities encountered difficulty in identifying the true management and beneficial ownership of the businesses.

In some cases, individuals listed as legal representatives were not traceable—meaning they could not be located in AADE’s registry.

Testimonies from employees also revealed that they either did not know the real owner of the business or received instructions by phone from unnamed individuals, while daily takings were handed over to persons unknown to them, following directions from individuals linked to the company.

A new audit methodology

The successful identification and dismantling of hundreds of offshoots of the network would not have been possible without a novel approach developed by the AADE. Through a vast web of connections and information, this approach enabled big-data analysis, targeted allocation of resources and audit actions, identification of strong nodes and critical corporate pathways, and evidence-based prioritization of subsets for further investigation and accountability.

According to these findings, the AADE applied a technologically innovative data-analysis and processing methodology that transformed a massive volume of administrative information into a structured network map.

The method included three core elements:

- data modeling and technical mapping of the network,

- identification of binary relationships (“exists/does not exist” relationships between entities),

- application of the Jaccard metric to measure degrees of similarity.

The system produced a network visualization of the rings, enabling targeted clustering of involved parties and prioritization of actions.

Three stages of analysis

The analysis was applied to 380 legal entities, regardless of whether they were active. From the consolidated mapping, 205 natural persons emerged as owners, shareholders, partners, or managers/legal representatives of these companies.

Processing followed three distinct stages:

- Mapping binary relationships: recording the co-appearance of individuals in any role across the 380 companies;

- Quantification using the Jaccard index: measuring the intensity and overlap of relationships between two individuals, based not only on the absolute number of shared companies but on the relative overlap of their corporate footprint;

- Network visualization and clustering: results led to visual identification of clusters and rings.

This methodology is now reproducible and can be used in future cases involving chains, multiple legal entities, multiple roles, and frequent changes.

How the fraud was set up

The operating model identified by the AADE displayed recurring characteristics:

- initially, members created companies and accumulated debts within specific legal entities;

- subsequently, they rendered those businesses inactive or effectively ceased operations without clearly documenting a shutdown;

- the fraud was completed through continuous succession of entities. The key was transferring activity from an old legal entity to a new one—often with the same or similar activity and, in some cases, at the same or nearby address.

In this way, the real beneficiaries continued operating undisturbed, leaving behind shell companies burdened with massive debts to the state and to the social-security fund (EFKA).

How the ring functioned

Using the innovative analysis methods, at least two individuals were identified as connected and collaborating, having coexisted within the same corporate structures as managers, members, partners, or shareholders.

The analysis showed that these shared participations were not random or sporadic but formed a stable pattern of repeated co-presence in corporate schemes.

Thus, three distinct sub-rings were uncovered:

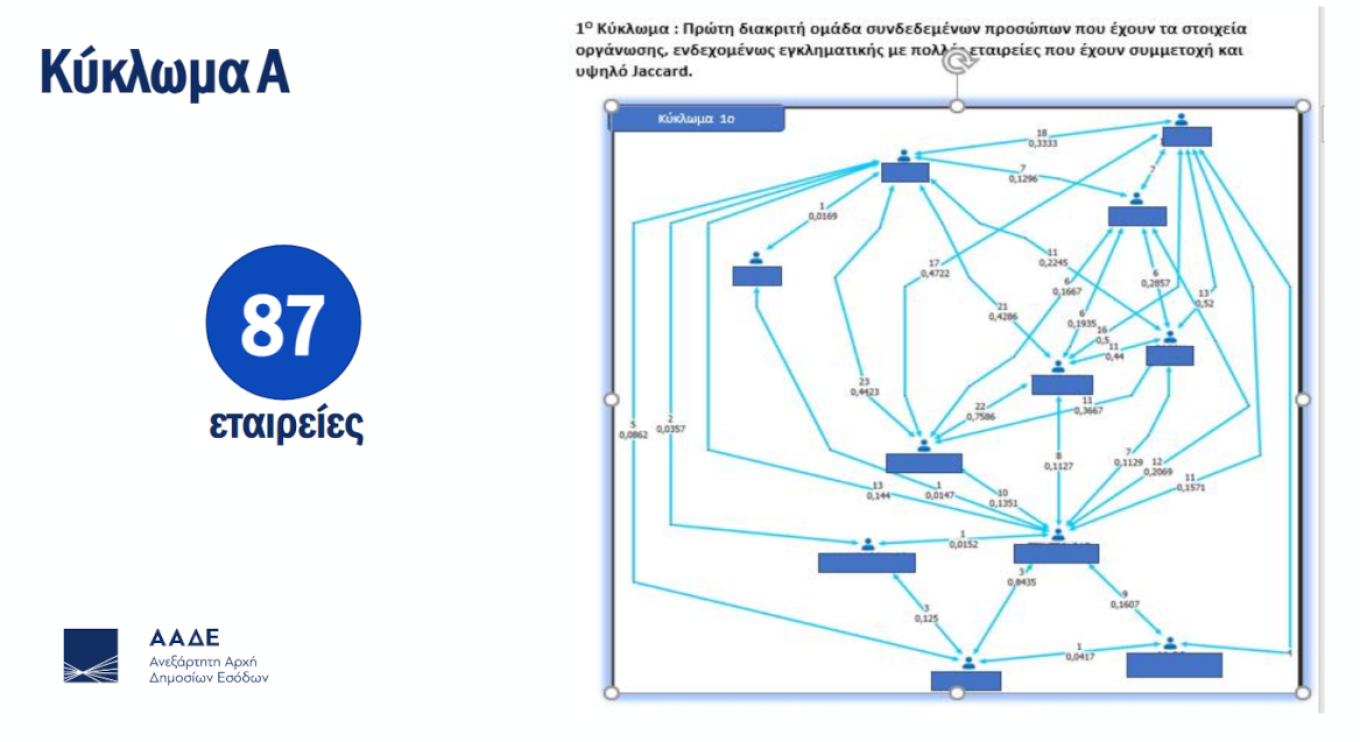

1. Ring A: the largest network

Ring A included 87 companies with debts of €11,396,587 in taxes and €6,164,946 in EFKA contributions—€17.56 million in total.

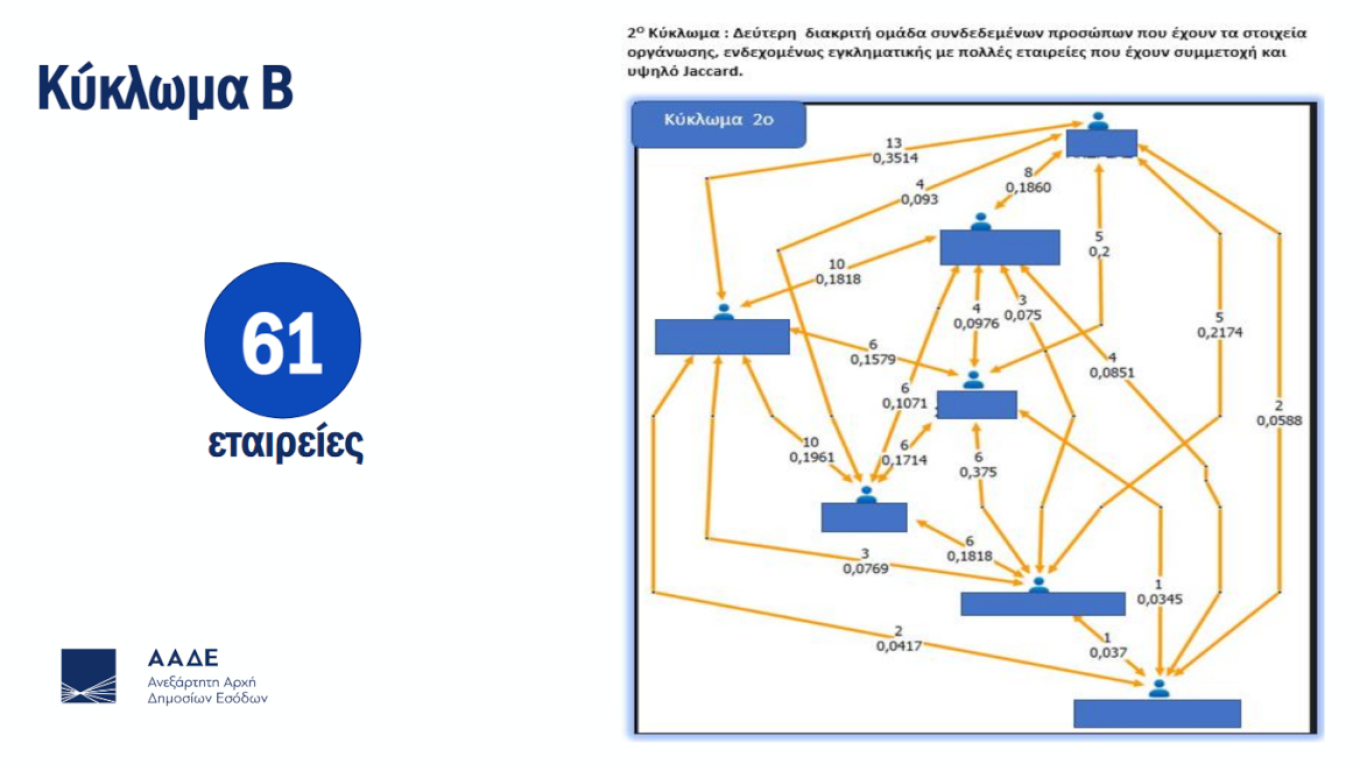

2. Ring B: the second-largest network

Ring B comprised 61 companies with debts of €1,790,875 in taxes and €1,810,472 in EFKA contributions—€3.6 million in total.

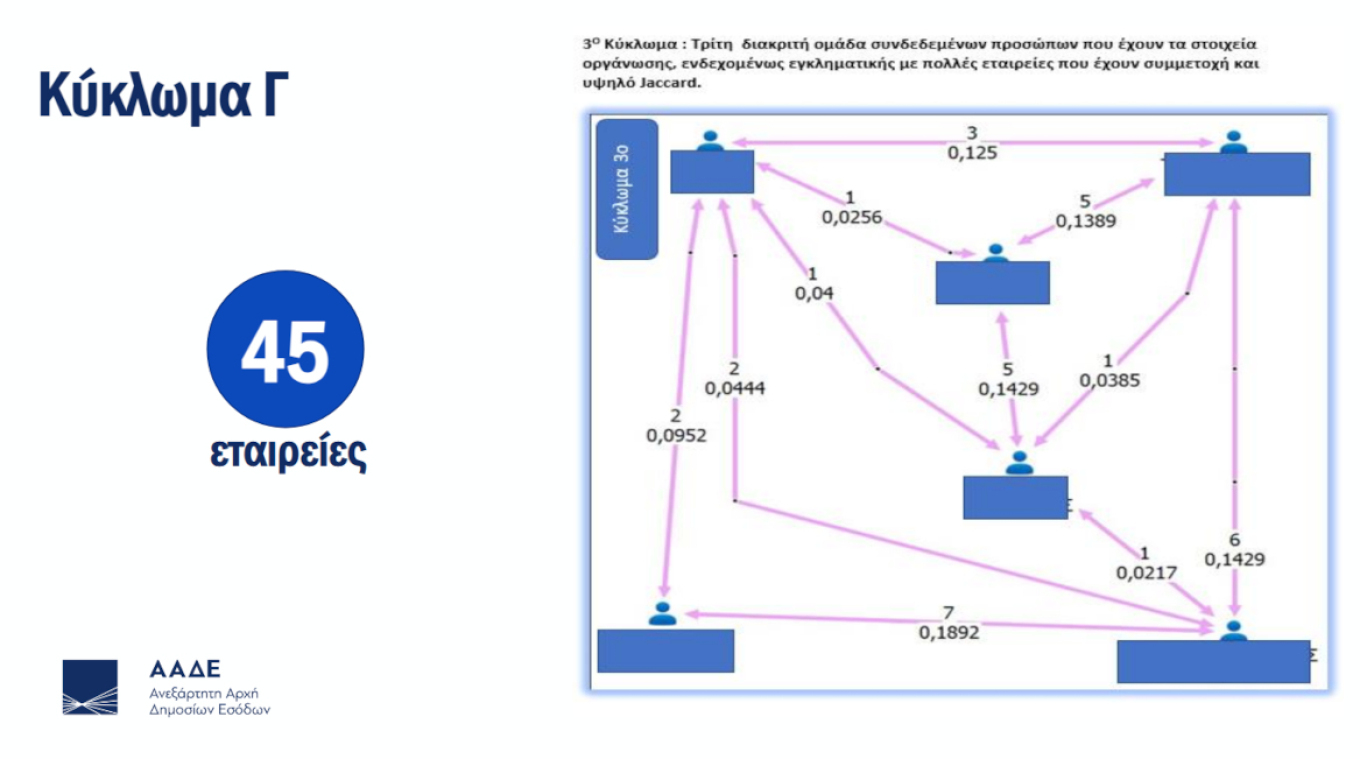

3. Ring C: the third (smaller) network

Ring C included 45 companies with debts of €2,416,466 in taxes and €1,030,120 in EFKA contributions—€3.45 million in total.

Ask me anything

Explore related questions